March’s Canadian labour market report was slightly softer than we expected, and the broader concern is that further weakness is still in the pipeline if the United States follows through with aggressive tariff hikes on global trade partners announced earlier this week.

Part of the pullback in employment (and tick higher in the unemployment rate) in March is likely already tied to intensifying international trade threats – manufacturing jobs fell for a second straight month. Other economic data has continued to look more resilient. Consumer spending has softened, but not nearly as much as consumer confidence that plunged to a record low in March.

The last round of U.S. reciprocal tariffs has mostly excluded Canada additional tariffs directly. But newly implemented (finished) auto tariffs could impact jobs in auto manufacturing and related sectors. Moreover, broader U.S. growth risks from much larger tariffs threatened to be imposed on imports from most of the rest of the world would spill over to negatively impact Canada as well.

In future meetings, the Bank of Canada will have to continue to balance the downside risks to the economy from international trade threats with the mandate to maintain a 2% inflation target, and we continue to assume that fiscal support will need to be the first line of defence to any trade driven economic shock.

Our current base case does not assume a race to the bottom for interest rates in Canada but does assume another cut in April.

The Details:

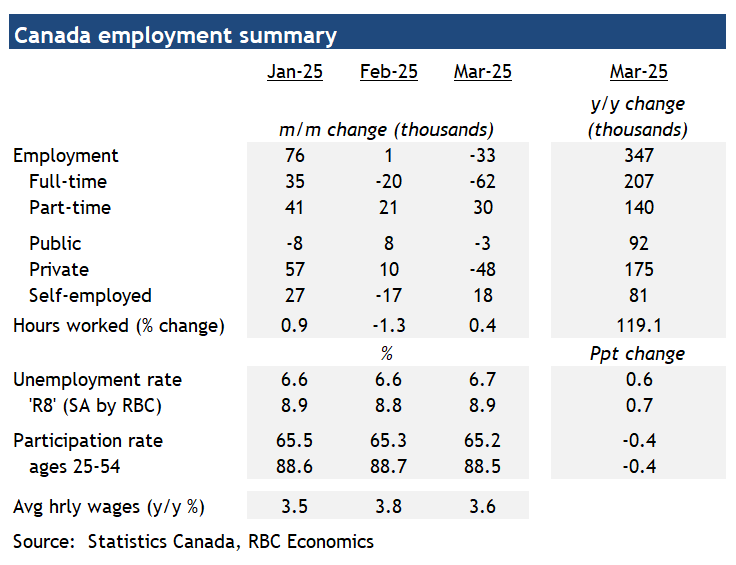

Employment fell 33k in March to push the unemployment rate higher to 6.7% (from 6.6% prior). Underlying details were soft – a larger 62k drop in full-time employment (on top of a 20k decline in February) was partially offset by a 30k increase in part-time work.

The increase in unemployment rate was despite another decline in labour force participation rate, down to 65.2% from 65.5% in January, and the first in four months. It was, however, still below the 6.9% recent peak in November last year. Actual hours worked partially bounced back in March (+0.4%) after severe snowstorms in February plunged the reading. Wage growth ticked lower, to 3.6% (year-over-year) given a smaller 0.2% monthly gain.

On an industry basis, the pullback in employment came from more domestically focused wholesale and retail trade (-29k) that retraced a little more than half the 51k surge in February. Information, culture and recreation also saw losses (-20k) while other service sectors recorded gains. There was a second small decline in manufacturing jobs in March (-7k). Employment in the sector will be watched closely in future jobs report, for signs of tariffs impacting labour conditions in Canada.

Going forward, slower population growth and rising uncertainty in international trade environment will continue to pose as headwinds to job growth. Job openings have persistently declined since January although to levels still above lows last year. We expect the unemployment rate in Canada will continue to edge higher this year.

source:https://thoughtleadership.rbc.com/canada-labour-market/